The headline grabbed you. Words like “Lost,” “Scammers,” “Retirement,” and “Savings” can do that. Adding a number didn’t hurt—”$740,000.”

This information recently appeared in a New York Times article about cybercriminals targeting Americans over 60. The wisdom of this targeting? These people have money—or, as the Times put it, “the largest pile of savings.”

This “pile” is also referred to as the largest transfer of wealth in history, referencing the assets accumulated by the Silent Generation and Baby Boomers. Like everyone else, they can’t take it with them. The amount to be passed down? Roughly $85 trillion. One more time for the folks in the back… $85,000,000,000,000.

As the Times established, this wealth makes for an appealing target. The elderly have long been subjected to scams. With a steady increase in cybercrime in general, the question arises: What protections exist to guard this money and ensure it gets to the rightful heir and/or the relevant tax authority?

Cybersecurity Expert Advocates for Greater Protections

Jason Makevich, founder and CEO of Greenlight Information Services, stressed the need for enhanced cybersecurity measures tailored to the needs of seniors. “Seniors should invest in solid cybersecurity protections and cyber awareness training to decrease their risk of being exploited,” he said. Makevich added, “They should also have a dedicated contact that they can reach out to for questions regarding any suspicious requests. In some cases, this may be a family member, but there should also be representatives at their financial institutions who are staffed and prepared to answer these questions.”

Makevich also called out financial institutions’ lack of involvement in protecting elderly customers. “Financial institutions have done everything possible to distance themselves from this risk, and while that is a shrewd business practice, they should come back toward the center on this,” he explained. He also notes, “Regulatory bodies such as FDIC and NCUA insure consumer deposits to a certain amount in the event of bank failure, but the institutions themselves are where the customers are placing their trust. Financial institutions should take a much more proactive role in educating their customers and their employees on the types of exploitation in their space.”

Makevich believes wealth managers should be the primary point of contact for those with substantial assets to prevent these losses. “For higher net worth individuals, their wealth manager should be well-versed in these types of scams and be a primary point of contact for their customers. For lower net worth individuals, these institutions should have (and publicize) a department dedicated to answering common questions and preventing these sorts of losses.”

Personal Cyber Insurance: An Emerging Solution?

Anna Brusco, Senior Vice President and National Product Development Leader at Marsh MMA Private Client Services highlighted the growing importance of personal cyber insurance in protecting individuals from cyber threats. “Personal cyber insurance came on the horizon about eight years ago as cybercrimes and attacks increased,” Brusco noted.

According to Brusco, the initial adopters of these policies were largely high-net-worth individuals and family offices who recognized that their financial assets and reputations were at stake. However, interest in these policies has expanded substantially over time. “Now, these issues and concerns have universal appeal as it becomes clearer every day that cyber exposure can impact anybody at any time,” she said.

Brusco emphasized that obtaining personal cyber insurance is not as tedious as securing commercial coverage. “When buying cyber coverage, you might be asked about your cyber hygiene practices or any past events, similar to being asked about your home security system when getting homeowners insurance,” she explained.

“Personal cyber insurance offers clients a lifeline. It helps them recover from a scary cyber situation, whether home devices are compromised, you’ve been tricked to part with money, or your computer’s been held hostage for ransomware,” Brusco added. “It also provides trusted resources such as cyber risk experts and legal professionals so you can get back to normal more quickly.”

Makevich sees personal cyber insurance as a potentially solid strategy to transfer risk, “Personal cyber insurance would certainly be a solid strategy to transfer risk and may be an untapped growth area.” However, he cautions that it may not suit everyone, “The everyday senior with $1 million or less that is budgeting for retirement may not have the liquidity to afford or justify the expense of this policy.”

Legislative Efforts to Protect Scam Victims

As cyber threats against the elderly escalate, legislative efforts are being made to provide relief to scam victims. The Tax Relief for Victims of Crimes, Scams, and Disasters Act seeks to reinstate the deductions for losses incurred by crime, which were eliminated by the 2018 Tax bill passed under the Trump administration. The bill is sponsored by Jim McGovern (MA-02) and Jamie Raskin (MD-08).

Congressman Jamie Raskin, who has been a vocal advocate for scam victims, tweeted in response to the Times Article: “Alas, stories like Barry’s are common as countless older Americans get targeted by scammers. I have a bill with @RepMcGovern to reinstate a tax deduction for scam victims like Barry to end tax punishment that adds insult to injury.”

The IRS currently treats a cashed-in IRA or 401k as income and expects a tax payment, even if the funds are stolen.

The FBI Sounds the Alarm

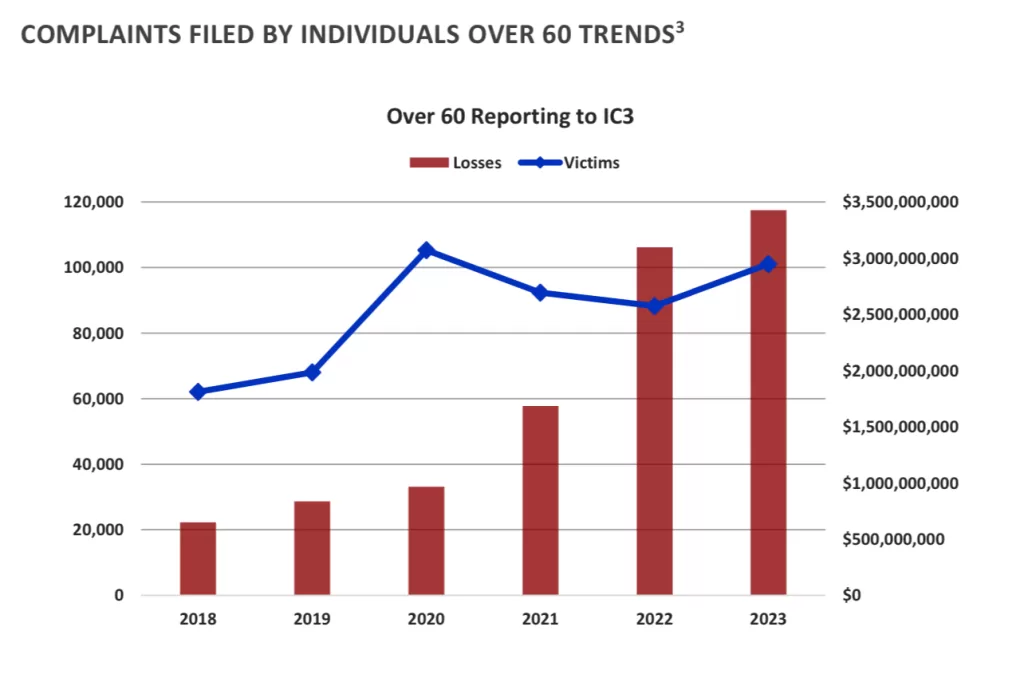

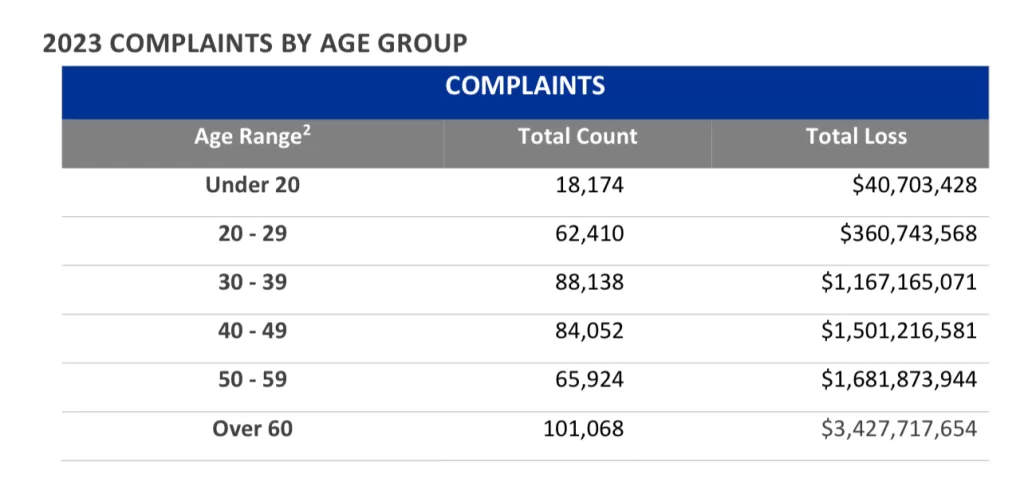

In 2023, the FBI’s Internet Crime Complaint Center (IC3) reported that those over 60 lost more than $3.4 billion to scams. That represents an 11% increase from 2022. Investment scams were the most costly, with losses exceeding $1.2 billion. The most common crime was tech support fraud, with victims over 60 losing almost $600 million.

The vulnerability of seniors is highlighted by call center scams, which the FBI says overwhelming targets them. Those over 60 lost almost $770 million in 2023, and those losses were greater than the losses of all other age groups combined. Beyond the financial losses, the FBI reports, victims have taken their lives as a result of “shame or loss of sustainable income.”

James Barnicle, head of the FBI’s Financial Crimes Section, urged financial institutions to protect elderly customers actively. “We think financial institutions do need to do more, to take some level of fiduciary responsibility and help protect their customers from being victims—especially in the elderly victim space,” Barnicle stated.

As the largest wealth transfer in history unfolds, the rising tide of cybercrime and scams targeting seniors underscores the urgent need for stronger cybersecurity protections for seniors.

Other News: Law Firms Go Unprotected From Cyber Crime(Opens in a new browser tab)

Other News: Hackers release reams of stolen Columbus data on dark web.