In an era where data breaches, cyberattacks, and cybersecurity dominate news, the vulnerabilities associated with intangible assets like intellectual property and artificial intelligence are becoming impossible to ignore. Businesses are finding that the threats they face are no longer just physical—they are digital, invisible, and often far more damaging. As companies continue to expand their digital footprints, they must confront the growing reality that traditional risk management strategies may no longer suffice.

The 2024 Intangible Versus Tangible Risks Comparison Report, sponsored by Aon and independently conducted by Ponemon Institute LLC, presents a critical analysis of the shifting landscape of risks faced by organizations globally. The report underscores the increasing importance of intangible assets, particularly in the realms of artificial intelligence (AI), intellectual property (IP), and cybersecurity. Below, we focus on key findings related to cybersecurity and cyber insurance. The full report is available here.

Cyber Risk Exposure Increases

Organizations worldwide are grappling with a surge in cyber risk exposure. According to the report, 56% of organizations experienced a material or significantly disruptive security exploit or data breach in the past 24 months. The financial impact of these incidents is staggering, with an average total cost of $5 million per incident. This spike in cyber incidents is driven by a combination of negligence, mistakes, and increasingly sophisticated cyberattacks that disrupt business operations and compromise sensitive information.

Moreover, the report reveals a growing awareness among organizations of the economic and legal ramifications of international data breaches. However, despite the heightened risk, a significant number of companies remain unprepared, with only 44% of respondents feeling confident in their ability to handle a potential “black swan” cyber event—an outlier incident with devastating consequences.

The Role of Cyber Insurance

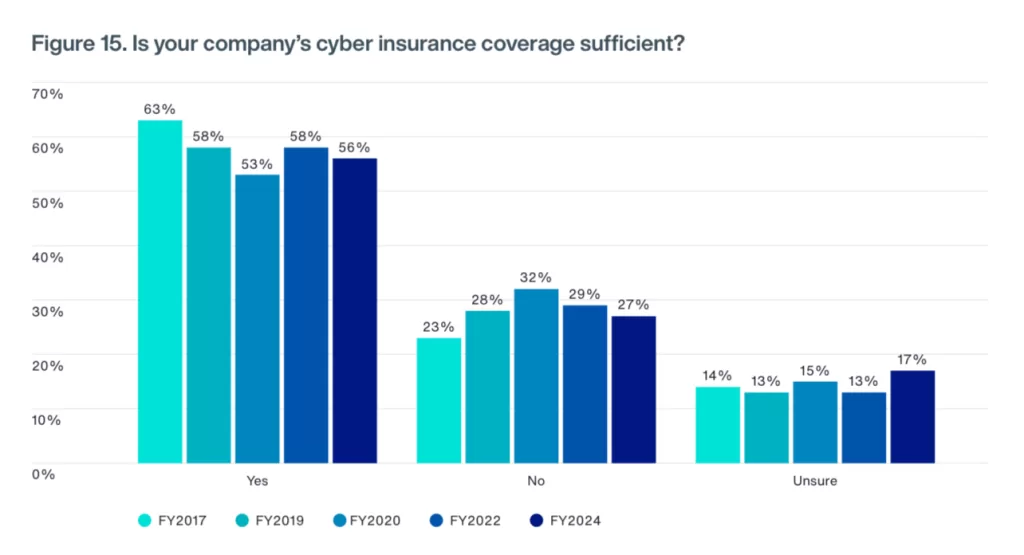

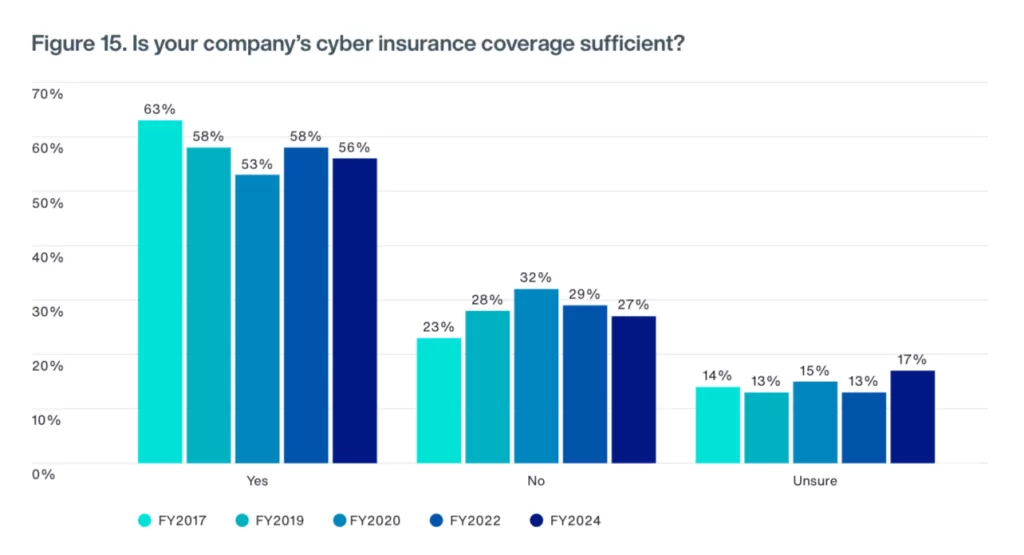

As cyber risks escalate, adopting cyber insurance as a risk mitigation tool is gaining traction, albeit slowly. The report highlights that while cyber liability is now recognized as a top 10 business risk, 70% of organizations still do not purchase standalone cyber insurance coverage. For those that do, the average insurance limit is set at $17 million, which, given the scale of potential losses, may be insufficient for covering catastrophic events.

One of the most striking findings is the limited scope of coverage provided by existing cyber insurance policies. Although 53% of data breaches are attributed to human error or negligence, only 33% of respondents report having insurance that covers such incidents. Additionally, few policies cover the costs associated with ransomware payments and recovery, leaving businesses vulnerable to significant financial losses in the event of an attack.

The Intersection of AI, IP, and Cybersecurity

The integration of AI into business operations has introduced new risks, particularly concerning intellectual property and cybersecurity. The report identifies that generative AI, while offering numerous benefits, also presents unique challenges, such as intellectual property infringement, security breaches, and misinformation. As these AI-driven risks grow, they complicate the landscape of cyber insurance, where traditional policies may not adequately address the nuanced exposures posed by AI technologies.

Moreover, the report emphasizes that most organizations lack comprehensive insurance coverage for IP-related incidents. Only 35% have a trade secret theft insurance policy, and an even smaller percentage have policies covering IP liabilities. This gap in coverage leaves companies exposed to potentially severe financial losses from IP theft or litigation, particularly as AI continues to evolve and influence IP landscapes.

The 2024 Intangible Versus Tangible Risks Comparison Report paints a clear picture of the escalating risks associated with intangible assets, particularly in cybersecurity and intellectual property. As businesses increasingly rely on AI and digital technologies, the need for robust cyber insurance and risk management strategies becomes more critical. However, the report suggests that many organizations still lag in adopting comprehensive insurance solutions, leaving them vulnerable to significant financial and reputational damage. Moving forward, companies must reassess their risk management frameworks and consider enhancing their cyber insurance coverage to safeguard against the growing threats in the digital landscape.

About the Report

The report was conducted by the Ponemon Institute LLC, a leading research organization focused on privacy, data protection, and information security policy. The consolidated sampling frame included 61,073 individuals across North America, EMEA, Asia-Pacific, and LATAM, all of whom are involved in their company’s cyber risk management and enterprise risk management activities. Out of the 2,671 respondents who completed the survey, 290 were rejected due to reliability issues, resulting in a final sample of 2,381 surveys, representing a 3.9 percent response rate.

Source: 2024 Intangible Versus Tangible Risks Comparison Report.

Other News: Coalition Touts New AI Tools for Cyber Insurance (Opens in a new browser tab)

Other News: Lawmaker calls for increased penalties for ransomware attacks against Michigan hospitals.