Estimated reading time: 4 minutes

A Growing Digital Battlefield

You know cyberattacks are escalating. Ransomware, phishing, and supply chain breaches now pose a significant threat to European corporations, SMEs, and banks. As digitization deepens and third-party service reliance grows, organizations face heightened exposure. Morningstar DBRS warns that this cyber vulnerability spans every industry. But the report notes cyber insurance is “a risk mitigating tool against enhanced cyber risks affecting corporates, small and medium-size enterprises (SMEs), and banks in Europe.” Consider this recent breach in April. Marks & Spencer and Co-op suffered combined losses of up to GBP 440 million. The European cyber landscape is growing increasingly hostile by the day.

Sector-Specific Threats

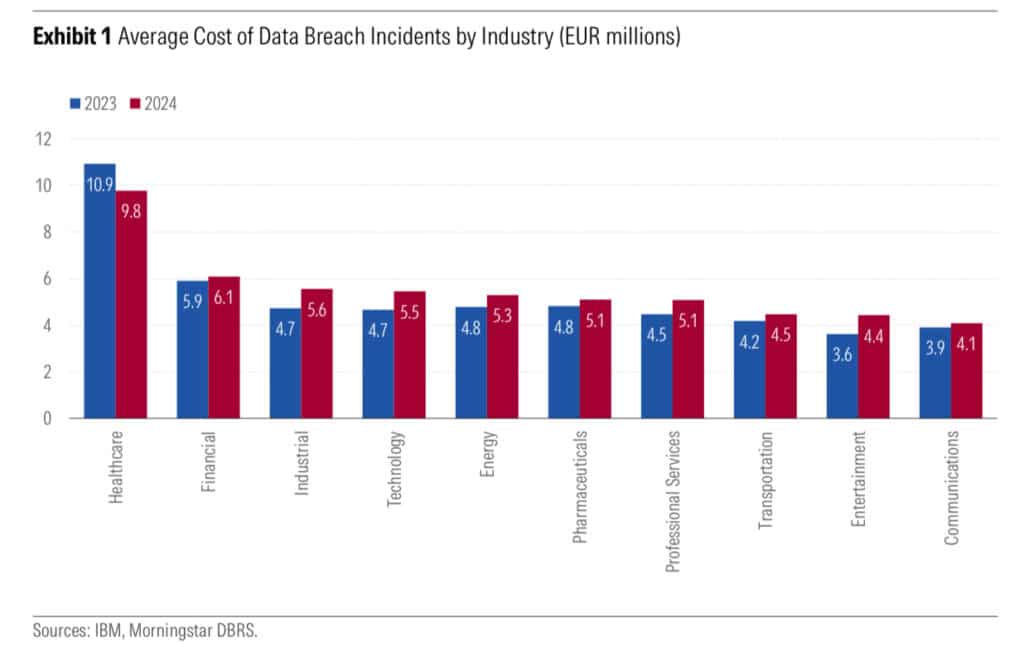

Data shows uneven distribution of cyberattacks. Healthcare and manufacturing suffer the most damaging ransomware events. Public administration also ranks high in frequency due to its ideological and geopolitical relevance. Meanwhile, sectors such as logistics and construction face risks due to interconnected supply chains.

IBM reported the average data breach cost globally at USD 4.88 million, with the EU’s range between USD 4.0 million and USD 5.9 million. The average cost of healthcare breaches topped USD 9.77 million.

Small Enterprises, Big Risks

SMEs remain dangerously exposed. They often lack IT departments and cyber budgets. Without alternatives, many pay ransoms, making them ideal targets. Successful attacks can shutter businesses entirely.

The 2023 NIS2 Directive raised the bar for cybersecurity compliance; however, implementation lags, particularly among mid-sized firms under financial strain.

Financial System Faces Instability

Banks now rank cyber risk as their leading threat. The Bank of England reported that 80% of financial institutions view cyber threats as a destabilizing factor. These threats extend beyond direct damage. Attacks ripple across interconnected financial systems.

The European Central Bank reported a 12% year-over-year increase in significant cyber incidents in 2024. Ransomware, DDoS attacks, and phishing remain the primary attack vectors. Rising geopolitical conflicts fuel politically motivated cyber strikes.

Cyber Insurance as a Financial Lifeline

“Cyber insurance can help mitigate financial losses generated by malicious and non-malicious cyber threats, especially for entities with limited defenses in place,” said Mario De Cicco, Vice President, Global Insurance and Pension Ratings at Morningstar DBRS.

Morningstar DBRS sees cyber insurance as a key strategic complement to internal defense systems. As firms brace for potential financial, legal, and reputational hits, insurance steps in as a safety net.

Skyrocketing Demand

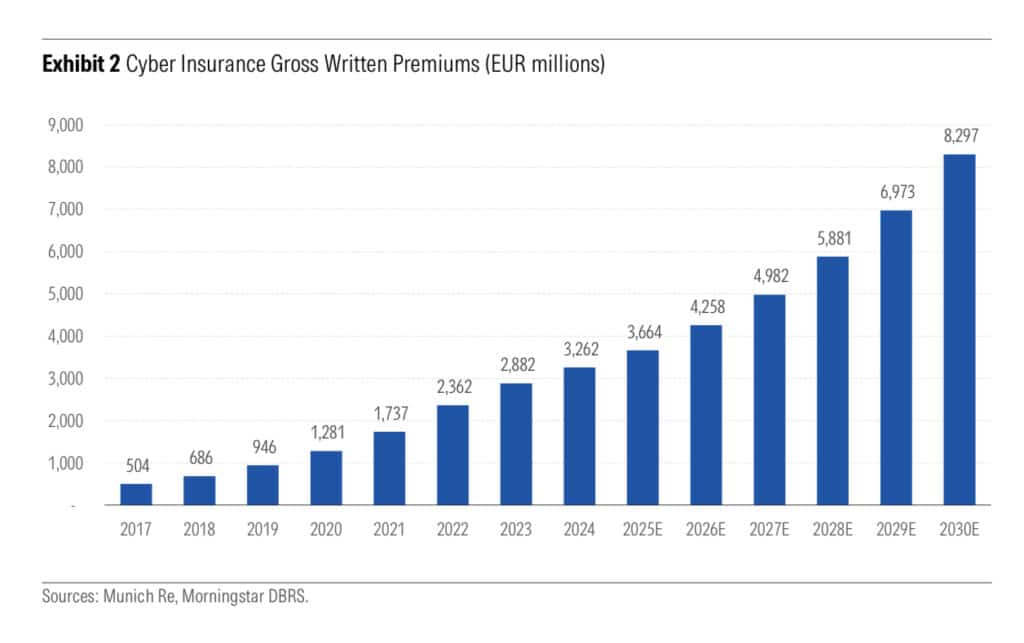

Cyber insurance premiums in Europe reached EUR 3.3 billion in 2024. That’s more than double the 2020 total. Global premiums hit EUR 15.3 billion last year, driven by rapid digitization and escalating cyber threats.

Demand is climbing. Premiums are expected to rise at a 14% compound annual growth rate, reaching EUR 8.3 billion in Europe by 2030.

A Market with Growing Pains

Despite growth, the European cyber insurance market remains underpenetrated. Premiums account for less than 1% of total property and casualty insurance. The sector is still maturing, with major players such as Beazley, Chubb, Munich Re, AXA, and Fairfax dominating it. These five control roughly 30% of global cyber insurance premiums.

The product itself is complex. As cyber threats evolve, insurers must continually reassess their risk models. The CrowdStrike update disaster in July 2024 resulted in global outages, leading to a 16% spike in cyber claims that year.

Claims Spike Challenges Insurers

Cyber claims rose 61% in 2024. Most were linked to network interruptions, data breaches, and extortion. New digital technologies and systemic interconnectivity continue to amplify the effects of cyber incidents.

The risks are real and potentially catastrophic. One cyber event can trigger global financial tremors. Insurers face the dual challenge of pricing products accurately while preparing for a surge in claims.

Listen to some prior reporting on the EU Cyber Insurance Scene

Outlook: Prepare or Perish

Morningstar DBRS sees a rapidly shifting cyber threat landscape. Regulations like DORA and NIS2 are tightening standards, but execution gaps persist. Cyber insurance stands as a necessary buffer, especially for vulnerable SMEs and exposed financial institutions.

As De Cicco emphasized, “Because of the dynamic nature of these risks, the fast-changing operating environment, and the potentially high financial impact of cyber events, (re)insurance companies need to prove their capability to effectively assess and price cyber risks.”