Natural disasters are easy to comprehend because the damage is visible, tangible, and emotionally striking; you can see the devastation and read the stories of lives lost. Cyberattacks, by contrast, lack this visceral impact—they unfold silently in digital spaces, often leaving no physical trace. But while they may seem less dramatic, cyber threats are no less damaging. In fact, beyond the incalculable human toll, which defies any price tag, the economic fallout from a digital disaster could be even greater than that of a catastrophic natural event.

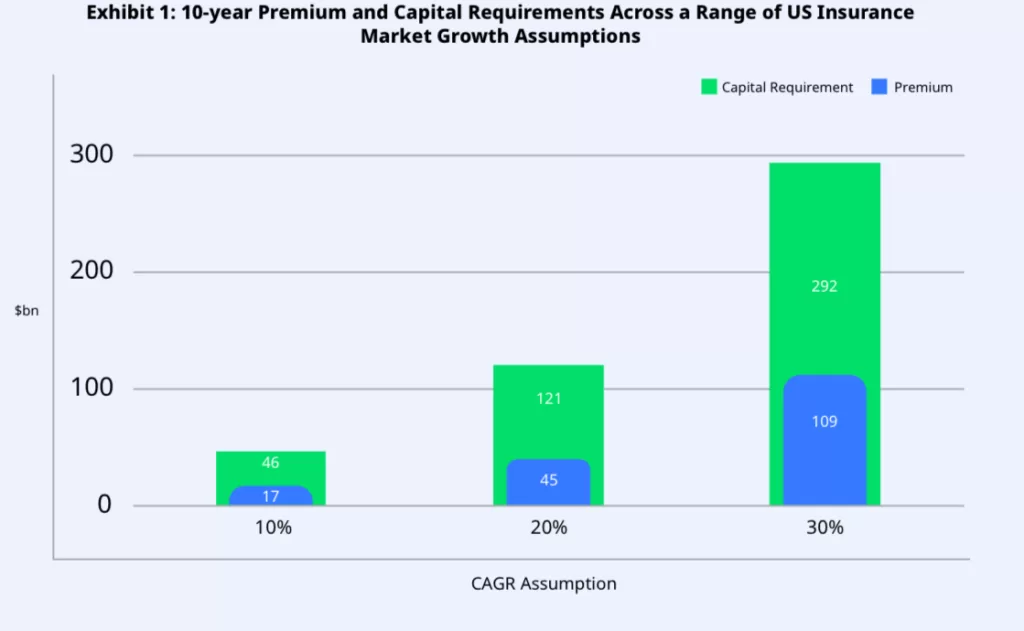

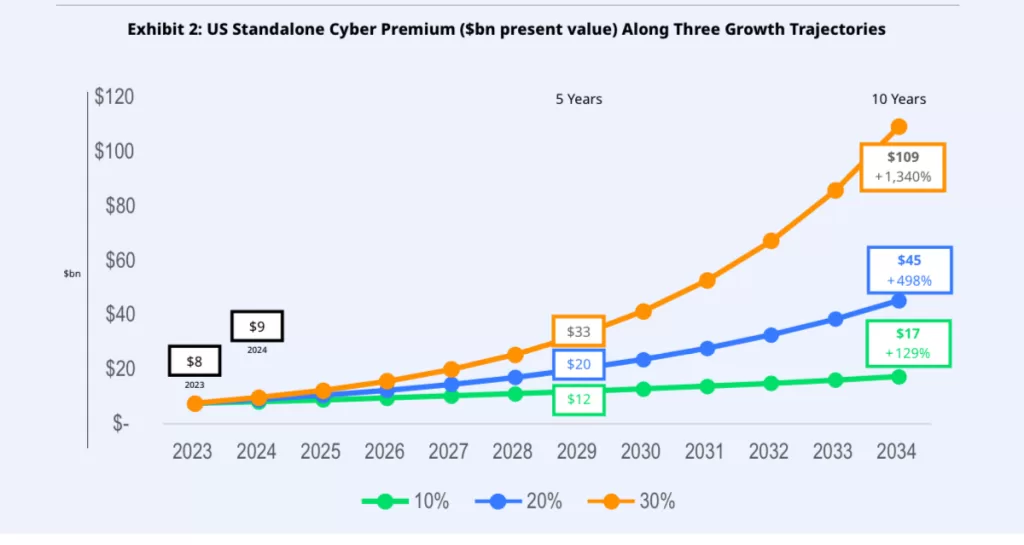

The cyber insurance sector is set to undergo a period of significant expansion, driven by an increasingly digital economy and escalating concerns about cyber threats. According to a new report by CyberCube, the U.S. cyber insurance market is poised for rapid growth over the next decade, with projections showing a potential increase in premiums ranging from $17 billion to $109 billion by 2034. However, realizing this growth will require substantial changes in capital allocation and structural innovation within the insurance sector.

Given the growing potential for cyber events to cause losses exceeding those of the most significant natural catastrophes, similar to Hurricane Katrina’s $102 billion impact, cyber insurance is becoming a peak peril for the property and casualty (P&C) insurance sector. At a moderate growth estimate of a 20% compound annual growth rate (CAGR), the capital required to manage a 1-in-250-year cyber event loss would soar to $121 billion—a substantial leap from the $20 billion required in 2023. The report underscores the need for the (re)insurance market to significantly boost its capital allocation to cover these burgeoning risks.

Our summary follows; you can get the full report here.

Challenges in Capital Allocation and Market Structuring

To sustain this growth trajectory, the (re)insurance market must diversify its capital sources, tapping into capital markets and potentially forming public-private partnerships. Insurance-linked securities (ILS), such as catastrophe bonds, are proposed as essential tools to absorb catastrophic tail risks, which currently pose a constraint on market growth.

While some progress has been made—evidenced by the issuance of $600 million in cyber catastrophe bonds by mid-2024—the market still lags behind the U.S. property ILS market, which stands at around $37 billion. Even if the cyber ILS market expands to match the property ILS market by 2034, CyberCube estimates that the insurance sector will need to increase its capital by over threefold in the next decade to meet the required levels.

Need for Product Innovation and Market Penetration

CyberCube’s findings highlight a pressing need for innovation in cyber insurance products to achieve real growth in insured exposures rather than relying solely on rate increases. Adoption rates for cyber insurance remain low, particularly among small and medium-sized enterprises (SMEs). While around 72% of large companies purchase some level of standalone cyber insurance, this number drops sharply to 43% for medium-sized companies, 12% for small businesses, and a mere 3% for micro-organizations.

To close these gaps, insurers and brokers must develop more comprehensive coverage options, offering more significant limits and more precise terms. Additionally, exploring new markets, such as consumer and microbusiness cyber insurance, alongside geographic and industry diversification, could help build premiums and spread risk away from peak catastrophe scenarios.

Structural Changes and Public-Private Partnerships

Given the potential for cyber events to result in losses surpassing those of the most significant natural disasters, akin to Hurricane Katrina, regulators and policymakers are urged to consider frameworks similar to those used for natural catastrophes. Public-private partnerships could provide essential backstops for extreme losses where private capital proves inadequate.

CyberCube’s analysis suggests that if the market achieves a 20% CAGR, the sector would need $121 billion in capital to manage peak risks—a fivefold increase over current levels. Partnerships between the government and the private sector, such as those seen with U.S. terrorism or flood risks, may be crucial to building resilience and mitigating catastrophic losses.

A Call for Greater Capital Efficiency and Risk Management

The report calls for improved capital efficiency and innovative risk management to fully realize the cyber insurance market’s growth potential. This includes diversification across geographies, new insurance products like personal cyber or cyber product liability, and advancements in reinsurance structuring. Enhanced cyber modeling approaches will also be critical in understanding and mitigating risks.

As digital threats grow in complexity and frequency, the demand for cyber insurance is expected to remain strong. However, the report cautions that achieving this growth will require concerted efforts across the insurance sector to innovate, diversify risk, and optimize capital allocation.

A Critical Juncture for the Cyber Insurance Market

CyberCube’s report concludes with a call to action for the insurance industry: to seize the opportunities presented by the growing demand for cyber insurance, the sector must implement structural changes and innovative solutions to manage risk effectively. By doing so, insurers can protect against increasingly severe cyber threats while fostering resilience in a digital-first world.

As cyber threats grow larger and more damaging, the next decade presents a pivotal moment for the cyber insurance market. If the sector can navigate the challenges of capital intensity and market structuring, it stands on the brink of unprecedented growth, ushering in a new era of protection for businesses against the ever-present risk of cyberattacks.

Source: Projecting Cyber Insurance Growth: A 10-Year US Market Outlook

Other News: City of Columbus sues researcher for sharing leaked ransomware data.